Mise à jour

Mise à jour de la base de données, veuillez patienter...

Site original : Krebs on Security

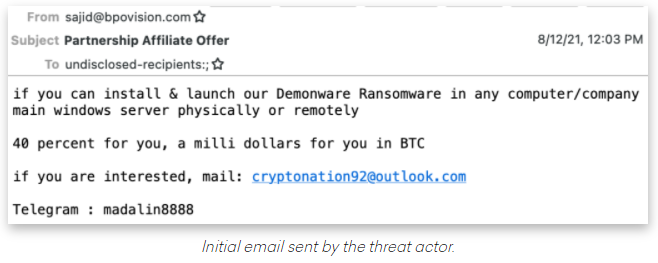

In August, KrebsOnSecurity warned that scammers were contacting people and asking them to unleash ransomware inside their employer’s network, in exchange for a percentage of any ransom amount paid by the victim company. This week, authorities in Nigeria arrested a suspect in connection with the scheme — a young man who said he was trying to save up money to help fund a new social network.

Image: Abnormal Security.

The brazen approach targeting disgruntled employees was first spotted by threat intelligence firm Abnormal Security, which described what happened after they adopted a fake persona and responded to the proposal in the screenshot above.

“According to this actor, he had originally intended to send his targets—all senior-level executives—phishing emails to compromise their accounts, but after that was unsuccessful, he pivoted to this ransomware pretext,” Abnormal’s Crane Hassold wrote.

Abnormal Security documented how it tied the email back to a Nigerian man who acknowledged he was trying to save up money to help fund a new social network he is building called Sociogram. In June 2021, the Nigerian government officially placed an indefinite ban on Twitter, restricting it from operating in Nigeria after the social media platform deleted tweets by the Nigerian president.

Reached via LinkedIn, Sociogram founder Oluwaseun Medayedupin asked to have his startup’s name removed from the story, although he did not respond to questions about whether there were any inaccuracies in Hassold’s report.

“Please don’t harm Sociogram’s reputation,” Medayedupin pleaded. “I beg you as a promising young man.”

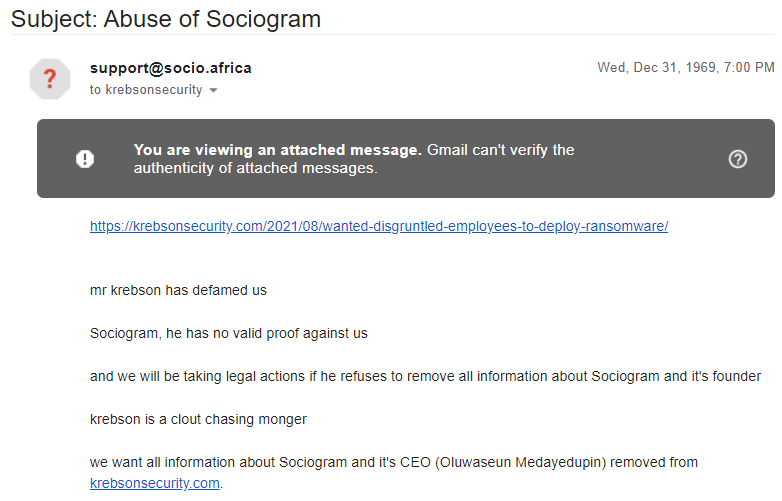

After he deleted his LinkedIn profile, I received the following message through the “contact this domain holder” link at KrebsOnSecurity’s domain registrar [curiously, the date of that missive reads “Dec. 31, 1969.”]. Apparently, Mr. Krebson is a clout-chasing monger.

A love letter from the founder of the ill-fated Sociogram.

Mr. Krebson also heard from an investigator representing the Nigeria Finance CERT on behalf of the Central Bank Of Nigeria. While the Sociogram founder’s approach might seem amateurish to some, the financial community in Nigeria did not consider it a laughing matter.

On Friday, police in Lagos arrested Medayedupin. The investigator says formal charges will be levied against the defendant sometime this week.

KrebsOnSecurity spoke with a fraud investigator who is performing the forensic analysis of the devices seized from Medayedupin’s home. The investigator spoke on condition of anonymity out of concern for his physical safety.

The investigator — we’ll call him “George” — said the 23-year-old Medayedupin lives with his extended family in an extremely impoverished home, and that the young man told investigators he’d just graduated from college but turned to cybercrime at first with ambitions of merely scamming the scammers.

George’s team confirmed that Medayedupin had around USD $2,000 to his name, which he’d recently stolen from a group of Nigerian fraudsters who were scamming people for gift cards. Apparently, he admitted to creating a phishing website that tricked a member of this group into providing access to the money they’d made from their scams.

Medayedupin reportedly told investigators that for almost a week after he started emailing his ransom-your-employer scheme, nobody took him up on the offer. But after his name appeared in the news media, he received thousands of inquiries from people interested in his idea.

George described Medayedupin as smart, a quick learner, and fairly dedicated to his work.

“He seems like he could be a fantastic [employee] for a company,” George said. “But there is no employment here, so he chose to do this.”

What’s interesting about this case — and indeed likely why anyone thought this guy worthy of arrest — is that the Nigerian authorities were fairly swift to take action when a domestic cybercriminal raised the specter of causing financial losses for its own banks.

After all, the majority of the cybercrime that originates from Africa — think romance scams, BEC fraud, and unemployment/pandemic loan fraud — does not target Nigerian citizens, nor does it harm African banks. On the contrary: This activity pumps a great deal of Western money into Nigeria.

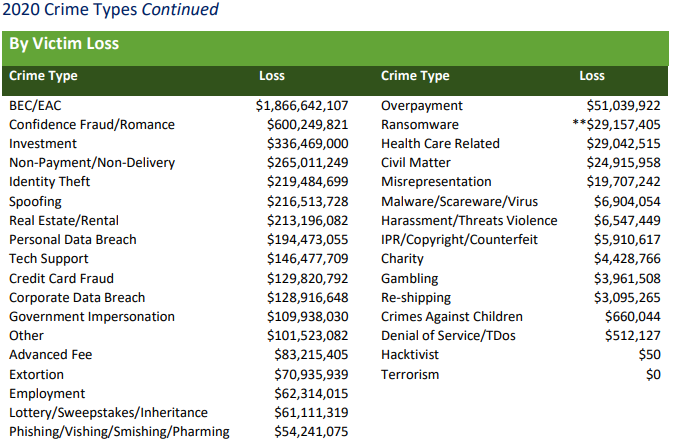

How much money are we talking about? The financial losses from these scams dwarf other fraud categories — such as identity theft or credit card fraud. According to the FBI’s Internet Crime Complaint Center (IC3), consumers and businesses reported more than $4.2 billion in losses tied to cybercrime in 2020, and BEC fraud and romance scams alone accounted for nearly 60 percent of those losses.

Source: FBI/IC3 2020 Internet Crime Report.

If the influx of a few billion US dollars into the Nigerian economy each year from cybercrime seems somehow insignificant, consider that (according to George) the average police officer in the country makes the equivalent of less than USD $100 a month.

Ronnie Tokazowski is a threat researcher at Agari, a security firm that has closely tracked many of the groups behind BEC scams. Tokazowski maintains he has been one of the more vocal proponents of the idea that trying to fight these problems by arresting those involved is something of a Sisyphean task, and that it makes way more sense to focus on changing the economic realities in places like Nigeria.

Nigeria has the world’s second-highest unemployment rate — rising from 27.1 percent in 2019 to 33 percent in 2020, according to the National Bureau of Statistics. The nation also is among the world’s most corrupt, according to 2020 findings from Transparency International.

“Education is definitely one piece, as raising awareness is hands down the best way to get ahead of this,” Tokazowski said, in a June 2021 interview. “But we also need to think about ways to create more business opportunities there so that people who are doing this to put food on the table have more legitimate opportunities. Unfortunately, thanks to the level of corruption of government officials, there are a lot of cultural reasons that fighting this type of crime at the source is going to be difficult.”

One of the more common ways cybercriminals cash out access to bank accounts involves draining the victim’s funds via Zelle, a “peer-to-peer” (P2P) payment service used by many financial institutions that allows customers to quickly send cash to friends and family. Naturally, a great deal of phishing schemes that precede these bank account takeovers begin with a spoofed text message from the target’s bank warning about a suspicious Zelle transfer. What follows is a deep dive into how this increasingly clever Zelle fraud scam typically works, and what victims can do about it.

Last week’s story warned that scammers are blasting out text messages about suspicious bank transfers as a pretext for immediately calling and scamming anyone who responds via text. Here’s what one of those scam messages looks like:

Anyone who responds “yes,” “no” or at all will very soon after receive a phone call from a scammer pretending to be from the financial institution’s fraud department. The caller’s number will be spoofed so that it appears to be coming from the victim’s bank.

To verify the identity of the customer, the fraudster asks for their online banking username, and then tells the customer to read back a passcode sent via text or email. In reality, the fraudster initiates a transaction — such as the “forgot password” feature on the financial institution’s site — which is what generates the 2-step authentication passcode delivered to the member.

Ken Otsuka is a senior risk consultant at CUNA Mutual Group, an insurance company that provides financial services to credit unions. Otsuka said a phone fraudster typically will say something like, “Before I get into the details, I need to verify that I’m speaking to the right person. What’s your username?”

“In the background, they’re using the username with the forgot password feature, and that’s going to generate one of these two-factor authentication passcodes,” Otsuka said. “Then the fraudster will say, ‘I’m going to send you the password and you’re going to read it back to me over the phone.'”

The fraudster then uses the code to complete the password reset process, and then changes the victim’s online banking password. The fraudster then uses Zelle to transfer the victim’s funds to others.

The fraudster then uses the code to complete the password reset process, and then changes the victim’s online banking password. The fraudster then uses Zelle to transfer the victim’s funds to others.

An important aspect of this scam is that the fraudsters never even need to know or phish the victim’s password. By sharing their username and reading back the one-time code sent to them via email, the victim is allowing the fraudster to reset their online banking password.

Otsuka said in far too many account takeover cases, the victim has never even heard of Zelle, nor did they realize they could move money that way.

“The thing is, many credit unions offer it by default as part of online banking,” Otsuka said. “Members don’t have to request to use Zelle. It’s just there, and with a lot of members targeted in these scams, although they’d legitimately enrolled in online banking, they’d never used Zelle before.” [Curious if your financial institution uses Zelle? Check out their partner list here].

Otsuka said credit unions offering other peer-to-peer banking products have also been targeted, but that fraudsters prefer to target Zelle due to the speed of the payments.

“The fraud losses can escalate quickly due to the sheer number of members that can be targeted on a single day over the course of consecutive days,” Otsuka said.

To combat this scam Zelle introduced out-of-band authentication with transaction details. This involves sending the member a text containing the details of a Zelle transfer – payee and dollar amount – that is initiated by the member. The member must authorize the transfer by replying to the text.

Unfortunately, Otsuka said, the scammers are defeating this layered security control as well.

“The fraudsters follow the same tactics except they may keep the members on the phone after getting their username and 2-step authentication passcode to login to the accounts,” he said. “The fraudster tells the member they will receive a text containing details of a Zelle transfer and the member must authorize the transaction under the guise that it is for reversing the fraudulent debit card transaction(s).”

In this scenario, the fraudster actually enters a Zelle transfer that triggers the following text to the member, which the member is asked to authorize: For example:

“Send $200 Zelle payment to Boris Badenov? Reply YES to send, NO to cancel. ABC Credit Union . STOP to end all messages.”

“My team has consulted with several credit unions that rolled Zelle out or our planning to introduce Zelle,” Otsuka said. “We found that several credit unions were hit with the scam the same month they rolled it out.”

The upshot of all this is that many financial institutions will claim they’re not required to reimburse the customer for financial losses related to these voice phishing schemes. Bob Sullivan, a veteran journalist who writes about fraud and consumer issues, says in many cases banks are giving customers incorrect and self-serving opinions after the thefts.

“Consumers — many who never ever realized they had a Zelle account – then call their banks, expecting they’ll be covered by credit-card-like protections, only to face disappointment and in some cases, financial ruin,” Sullivan wrote in a recent Substack post. “Consumers who suffer unauthorized transactions are entitled to Regulation E protection, and banks are required to refund the stolen money. This isn’t a controversial opinion, and it was recently affirmed by the CFPB here. If you are reading this story and fighting with your bank, start by providing that link to the financial institution.”

“If a criminal initiates a Zelle transfer — even if the criminal manipulates a victim into sharing login credentials — that fraud is covered by Regulation E, and banks should restore the stolen funds,” Sullivan said. “If a consumer initiates the transfer under false pretenses, the case for redress is more weak.”

Sullivan notes that the Consumer Financial Protection Bureau (CFPB) recently announced it was conducting a probe into companies operating payments systems in the United States, with a special focus on platforms that offer fast, person-to-person payments.

“Consumers expect certain assurances when dealing with companies that move their money,” the CFPB said in its Oct. 21 notice. “They expect to be protected from fraud and payments made in error, for their data and privacy to be protected and not shared without their consent, to have responsive customer service, and to be treated equally under relevant law. The orders seek to understand the robustness with which payment platforms prioritize consumer protection under law.”

Anyone interested in letting the CFPB know about a fraud scam that abused a P2P payment platform like Zelle, Cashapp, or Venmo, for example, should send an email describing the incident to BigTechPaymentsInquiry@cfpb.gov. Be sure to include Docket No. CFPB-2021-0017 in the subject line of the message.

In the meantime, remember the mantra: Hang up, Look Up, and Call Back. If you receive a call from someone warning about fraud, hang up. If you believe the call might be legitimate, look up the number of the organization supposedly calling you, and call them back.

The CEO of a South Carolina technology firm has pleaded guilty to 20 counts of wire fraud in connection with an elaborate network of phony companies set up to obtain more than 735,000 Internet Protocol (IP) addresses from the nonprofit organization that leases the digital real estate to entities in North America.

In 2018, the American Registry for Internet Numbers (ARIN), which oversees IP addresses assigned to entities in the U.S., Canada, and parts of the Caribbean, notified Charleston, S.C. based Micfo LLC that it intended to revoke 735,000 addresses.

ARIN said they wanted the addresses back because the company and its owner — 38-year-old Amir Golestan — had obtained them under false pretenses. A global shortage of IPv4 addresses has massively driven up the price of these resources over the years: At the time of this dispute, a single IP address could fetch between $15 and $25 on the open market.

Micfo responded by suing ARIN to try to stop the IP address seizure. Ultimately, ARIN and Micfo settled the dispute in arbitration, with Micfo returning most of the addresses that it hadn’t already sold.

But the legal tussle caught the attention of South Carolina U.S. Attorney Sherri Lydon, who in May 2019 filed criminal wire fraud charges against Golestan, alleging he’d orchestrated a network of shell companies and fake identities to prevent ARIN from knowing the addresses were all going to the same buyer.

Each of those shell companies involved the production of notarized affidavits in the names of people who didn’t exist. As a result, Lydon was able to charge Golestan with 20 counts of wire fraud — one for each payment made by the phony companies that bought the IP addresses from ARIN.

Amir Golestan, CEO of Micfo.

On Nov. 16, just two days into his trial, Golestan changed his “not guilty” plea, agreeing to plead guilty to all 20 wire fraud charges. KrebsOnSecurity interviewed Golestan at length earlier this year, but he has not responded to requests for comment on his plea change.

By 2013, a number of Micfo’s customers had landed on the radar of Spamhaus, a group that many network operators rely upon to help block junk email. But shortly after Spamhaus began blocking many of Micfo’s IP address ranges, Micfo shifted gears and began reselling IP addresses mainly to companies marketing “virtual private networking” or VPN services that help customers hide their real IP addresses online.

In a 2020 interview, Golestan told KrebsOnSecurity that Micfo was at one point responsible for brokering roughly 40 percent of the IP addresses used by the world’s largest VPN providers. Throughout that conversation, Golestan maintained his innocence, even as he explained that the creation of the phony companies was necessary to prevent entities like Spamhaus from interfering with its business going forward.

Stephen Ryan, an attorney representing ARIN, said Golestan changed his plea after the court heard from a former Micfo employee and public notary who described being instructed by Golestan to knowingly certify false documents.

“Her testimony made him appear bullying and unsavory,” Ryan said. “Because it turned out he had also sued her to try to prevent her from disclosing the actions he’d directed.”

Golestan’s rather sparse plea agreement (first reported by The Wall Street Journal) does not specify any sort of leniency he might gain from prosecutors for agreeing to end the trial prematurely. But it’s worth noting that a conviction on a single act of wire fraud can result in fines and up to 20 years in prison.

The courtroom drama comes as ARIN’s counterpart in Africa is embroiled in a similar, albeit much larger dispute over millions of wayward African IP addresses. In July 2021, the African Network Information Centre (AFRINIC) confiscated more than six million IP addresses from Cloud Innovation, a company incorporated in the African offshore entity haven of Seychelles (pronounced, quite aptly — “say shells”).

AFRINIC revoked the addresses — valued at around USD $120 million — after an internal review found that most of them were being used outside of Africa by various entities in China and Hong Kong. Like ARIN, AFRINIC’s policies require those who are leasing IP addresses to demonstrate that the addresses are being used by entities within their geographic region.

But just weeks later, Cloud Innovation convinced a judge in AFRINIC’s home country of Mauritius to freeze $50 million in AFRINIC bank accounts, arguing that AFRINIC had “acted in bad faith and upon frivolous grounds to tarnish the reputation of Cloud Innovation,” and that it was obligated to protect its customers from disruption of service.

That financial freeze has since been partially lifted, but the legal and financial wrangling between AFRINIC and Cloud Innovation continues. The company’s CEO is also suing the CEO and board chair of AFRINIC in an $80 million defamation case.

Ron Guilmette is a security researcher who spent several years tracing how tens of millions of dollars worth of AFRINIC IP addresses were privately sold to address brokers by a former AFRINIC executive. Guilmette said Golestan’s guilty plea is a positive sign for AFRINIC, ARIN and the three other Regional Internet Registries (RIRs).

“It’s good news for the rule of law,” Guilmette said. “It has implications for the AFRINIC case because it reaffirms the authority of all RIRs, including AFRINIC and ARIN.”

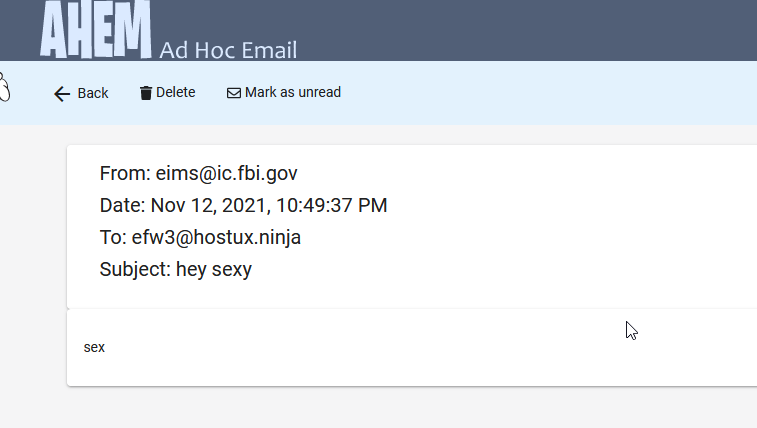

The Federal Bureau of Investigation (FBI) confirmed today that its fbi.gov domain name and Internet address were used to blast out thousands of fake emails about a cybercrime investigation. According to an interview with the person who claimed responsibility for the hoax, the spam messages were sent by abusing insecure code in an FBI online portal designed to share information with state and local law enforcement authorities.

The phony message sent late Thursday evening via the FBI’s email system. Image: Spamhaus.org

Late in the evening of Nov. 12 ET, tens of thousands of emails began flooding out from the FBI address eims@ic.fbi.gov, warning about fake cyberattacks. Around that time, KrebsOnSecurity received an email from the same email address.

“Hi its pompompurin,” read the message. “Check headers of this email it’s actually coming from FBI server. I am contacting you today because we located a botnet being hosted on your forehead, please take immediate action thanks.”

A review of the email’s message headers indicated it had indeed been sent by the FBI, and from the agency’s own Internet address. The domain in the “from:” portion of the email I received — eims@ic.fbi.gov — corresponds to the FBI’s Criminal Justice Information Services division (CJIS).

According to the Department of Justice, “CJIS manages and operates several national crime information systems used by the public safety community for both criminal and civil purposes. CJIS systems are available to the criminal justice community, including law enforcement, jails, prosecutors, courts, as well as probation and pretrial services.”

In response to a request for comment, the FBI confirmed the unauthorized messages, but declined to offer further information.

“The FBI and CISA [the Cybersecurity and Infrastructure Security Agency] are aware of the incident this morning involving fake emails from an @ic.fbi.gov email account,” reads the FBI statement. “This is an ongoing situation and we are not able to provide any additional information at this time. The impacted hardware was taken offline quickly upon discovery of the issue. We continue to encourage the public to be cautious of unknown senders and urge you to report suspicious activity to www.ic3.gov or www.cisa.gov.”

In an interview with KrebsOnSecurity, Pompompurin said the hack was done to point out a glaring vulnerability in the FBI’s system.

“I could’ve 1000% used this to send more legit looking emails, trick companies into handing over data etc.,” Pompompurin said. “And this would’ve never been found by anyone who would responsibly disclose, due to the notice the feds have on their website.”

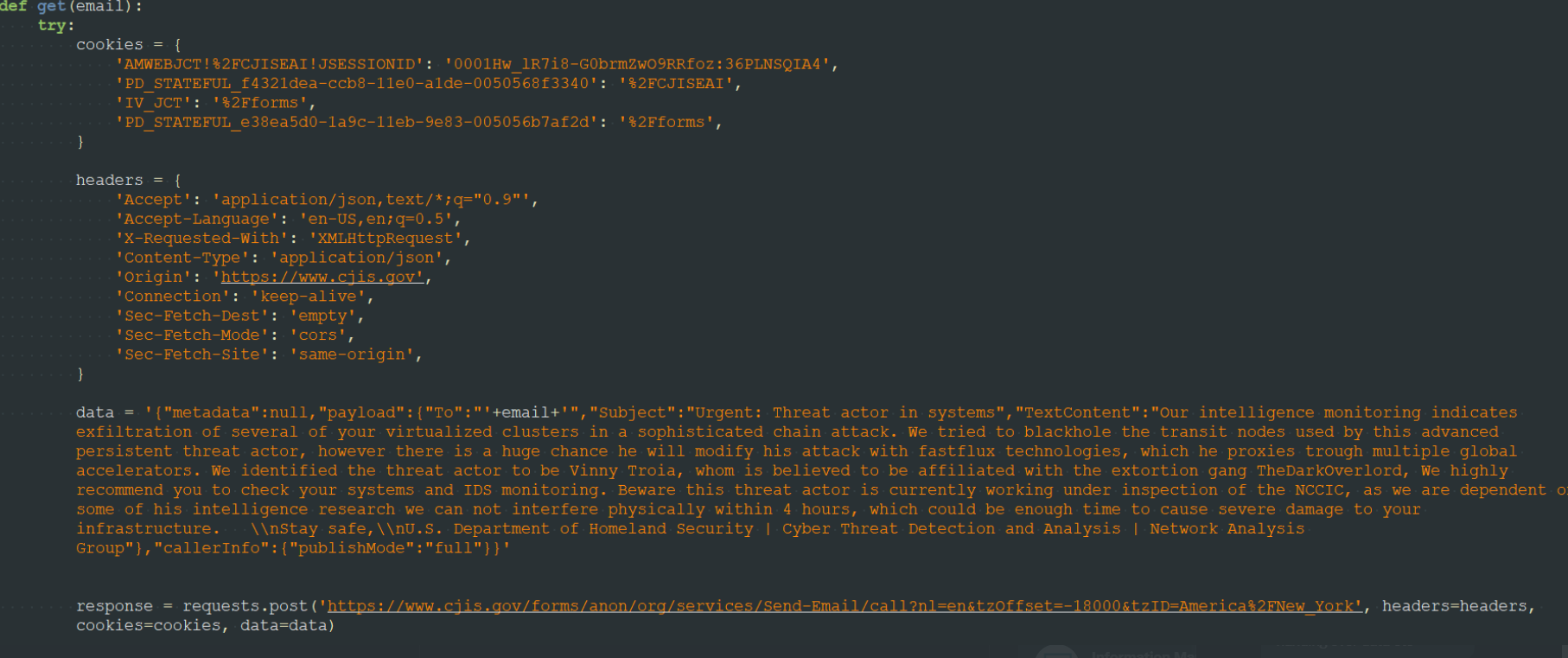

Pompompurin says the illicit access to the FBI’s email system began with an exploration of its Law Enforcement Enterprise Portal (LEEP), which the agency describes as “a gateway providing law enforcement agencies, intelligence groups, and criminal justice entities access to beneficial resources.”

The FBI’s Law Enforcement Enterprise Portal (LEEP).

“These resources will strengthen case development for investigators, enhance information sharing between agencies, and be accessible in one centralized location!,” the FBI’s site enthuses.

Until sometime this morning, the LEEP portal allowed anyone to apply for an account. Helpfully, step-by-step instructions for registering a new account on the LEEP portal also are available from the DOJ’s website. [It should be noted that “Step 1” in those instructions is to visit the site in Microsoft’s Internet Explorer, an outdated web browser that even Microsoft no longer encourages people to use for security reasons.]

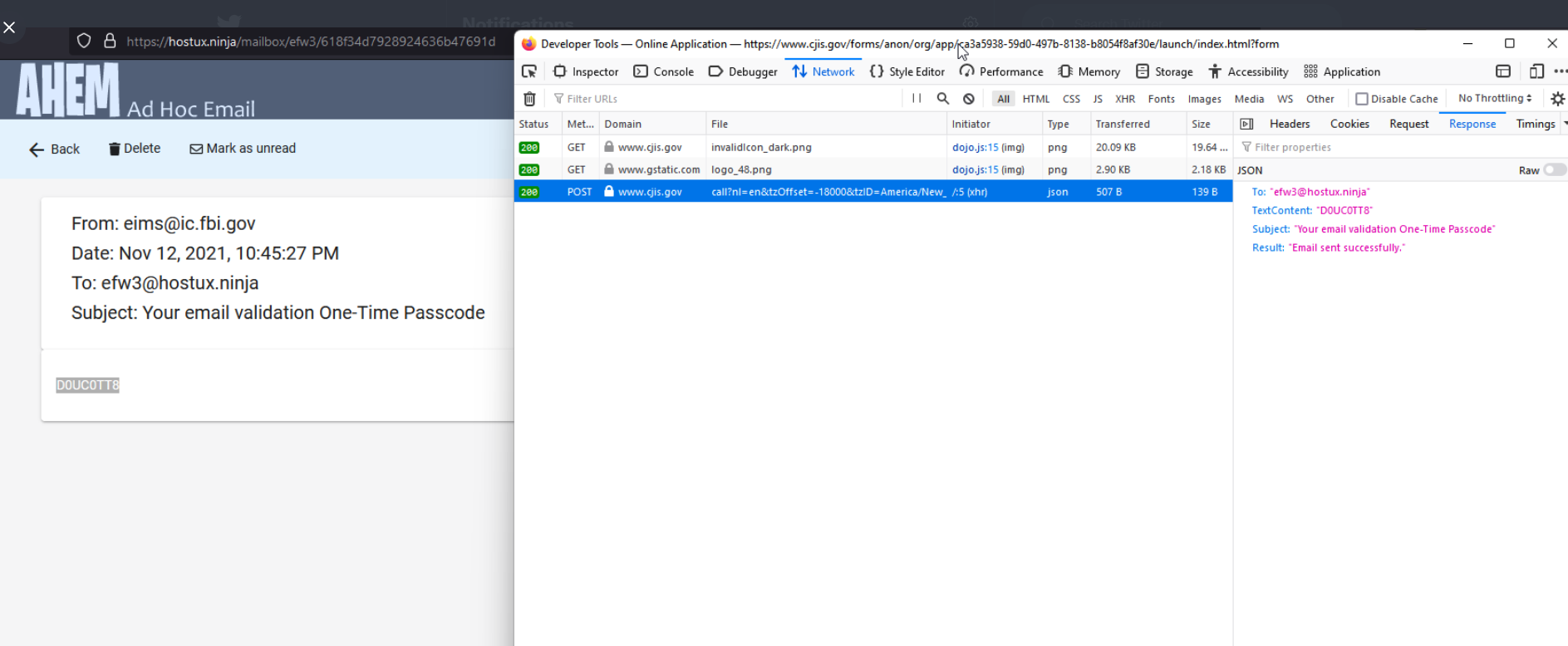

Much of that process involves filling out forms with the applicant’s personal and contact information, and that of their organization. A critical step in that process says applicants will receive an email confirmation from eims@ic.fbi.gov with a one-time passcode — ostensibly to validate that the applicant can receive email at the domain in question.

But according to Pompompurin, the FBI’s own website leaked that one-time passcode in the HTML code of the web page.

A screenshot shared by Pompompurin. Image: KrebOnSecurity.com

Pompompurin said they were able to send themselves an email from eims@ic.fbi.gov by editing the request sent to their browser and changing the text in the message’s “Subject” field and “Text Content” fields.

A test email using the FBI’s communications system that Pompompurin said they sent to a disposable address.

“Basically, when you requested the confirmation code [it] was generated client-side, then sent to you via a POST Request,” Pompompurin said. “This post request includes the parameters for the email subject and body content.”

Pompompurin said a simple script replaced those parameters with his own message subject and body, and automated the sending of the hoax message to thousands of email addresses.

A screenshot shared by Pompompurin, who says it shows how he was able to abuse the FBI’s email system to send a hoax message.

“Needless to say, this is a horrible thing to be seeing on any website,” Pompompurin said. “I’ve seen it a few times before, but never on a government website, let alone one managed by the FBI.”

As we can see from the first screenshot at the top of this story, Pompompurin’s hoax message is an attempt to smear the name of Vinny Troia, the founder of the dark web intelligence companies NightLion and Shadowbyte.

“Members of the RaidForums hacking community have a long standing feud with Troia, and commonly deface websites and perform minor hacks where they blame it on the security researcher,” Ionut Illascu wrote for BleepingComputer. “Tweeting about this spam campaign, Vinny Troia hinted at someone known as ‘pompompurin,’ as the likely author of the attack. Troia says the individual has been associated in the past with incidents aimed at damaging the security researcher’s reputation.”

Troia’s work as a security researcher was the subject of a 2018 article here titled, “When Security Researchers Pose as Cybercrooks, Who Can Tell the Difference?” No doubt this hoax was another effort at blurring that distinction.

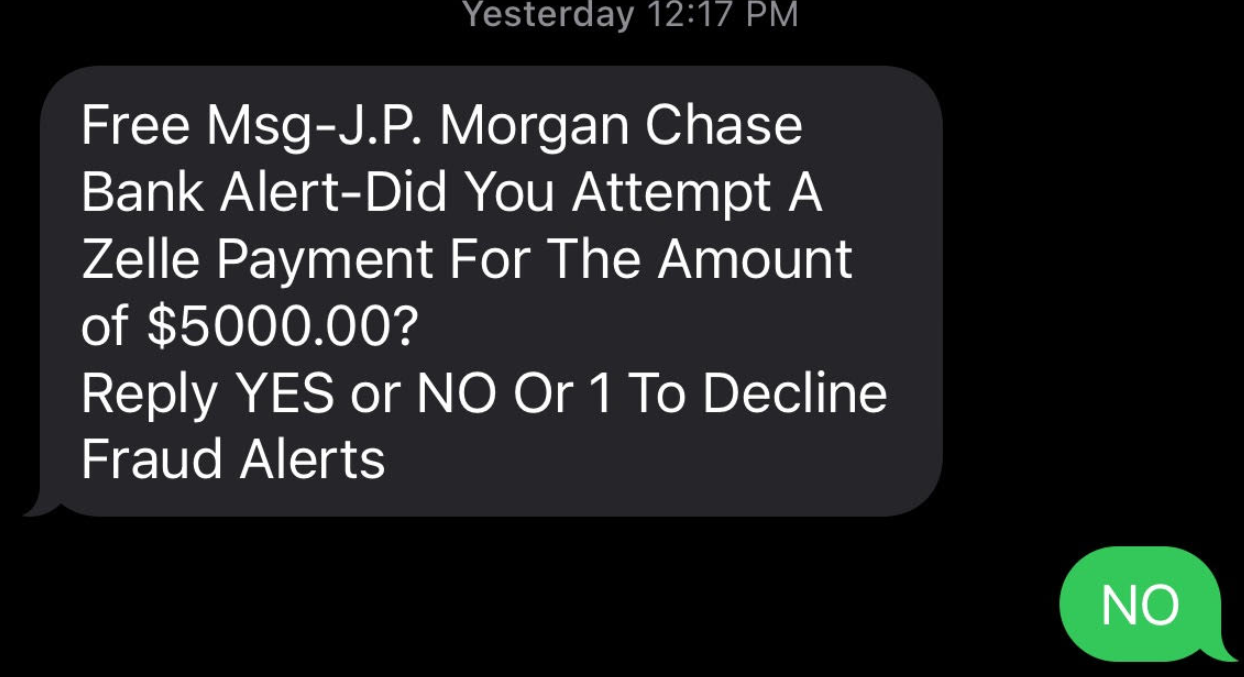

Most of us have probably heard the term “smishing” — which is a portmanteau for traditional phishing scams sent through SMS text messages. Smishing messages usually include a link to a site that spoofs a popular bank and tries to siphon personal information. But increasingly, phishers are turning to a hybrid form of smishing — blasting out linkless text messages about suspicious bank transfers as a pretext for immediately calling and scamming anyone who responds via text.

KrebsOnSecurity recently heard from a reader who said his daughter received an SMS that said it was from her bank, and inquired whether she’d authorized a $5,000 payment from her account. The message said she should reply “Yes” or “No,” or 1 to decline future fraud alerts.

Since this seemed like a reasonable and simple request — and she indeed had an account at the bank in question — she responded, “NO.”

Seconds later, her mobile phone rang.

“When she replied ‘no,’ someone called immediately, and the caller ID said ‘JP Morgan Chase’,” reader Kris Stevens told KrebsOnSecurity. “The person on the phone said they were from the fraud department and they needed to help her secure her account but needed information from her to make sure they were talking to the account owner and not the scammer.”

Thankfully, Stevens said his daughter had honored the gold rule regarding incoming phone calls about fraud: When In Doubt, Hang up, Look up, and Call Back.

“She knows the drill so she hung up and called Chase, who confirmed they had not called her,” he said. “What was different about this was it was all very smooth. No foreign accents, the pairing of the call with the text message, and the fact that she does have a Chase account.”

The remarkable aspect of these phone-based phishing scams is typically the attackers never even try to log in to the victim’s bank account. The entirety of the scam takes place over the phone.

We don’t know what the fraudsters behind this clever hybrid SMS/voice phishing scam intended to do with the information they might have coaxed from Stevens’ daughter. But in previous stories and reporting on voice phishing schemes, the fraudsters used the phished information to set up new financial accounts in the victim’s name, which they then used to receive and forward large wire transfers of stolen funds.

Even many security-conscious people tend to focus on protecting their online selves, while perhaps discounting the threat from less technically sophisticated phone-based scams. In 2020 I told the story of “Mitch” — the tech-savvy Silicon Valley executive who got voice phished after he thought he’d turned the tables on the scammers.

Unlike Stevens’ daughter, Mitch didn’t hang up with the suspected scammers. Rather, he put them on hold. Then Mitch called his bank on the other line and asked if their customer support people were in fact engaged in a separate conversation with him over the phone.

The bank replied that they were indeed speaking to the same customer on a different line at that very moment. Feeling better, Mitch got back on the line with the scammers. What Mitch couldn’t have known at that point was that a member of the fraudster’s team simultaneously was impersonating him on the phone with the bank’s customer service people.

So don’t be Mitch. Don’t try to outsmart the crooks. Just remember this anti-fraud mantra, and maybe repeat it a few times in front of your friends and family: When in doubt, hang up, look up, and call back. If you believe the call might be legitimate, look up the number of the organization supposedly calling you, and call them back.

And I suppose the same time-honored advice about not replying to spam email goes doubly for unsolicited text messages: When in doubt, it’s best not to respond.